Report: Improper Obamacare Payments Could Reach $25B in 2026

06/06/2026 / By Morgan S. Verity

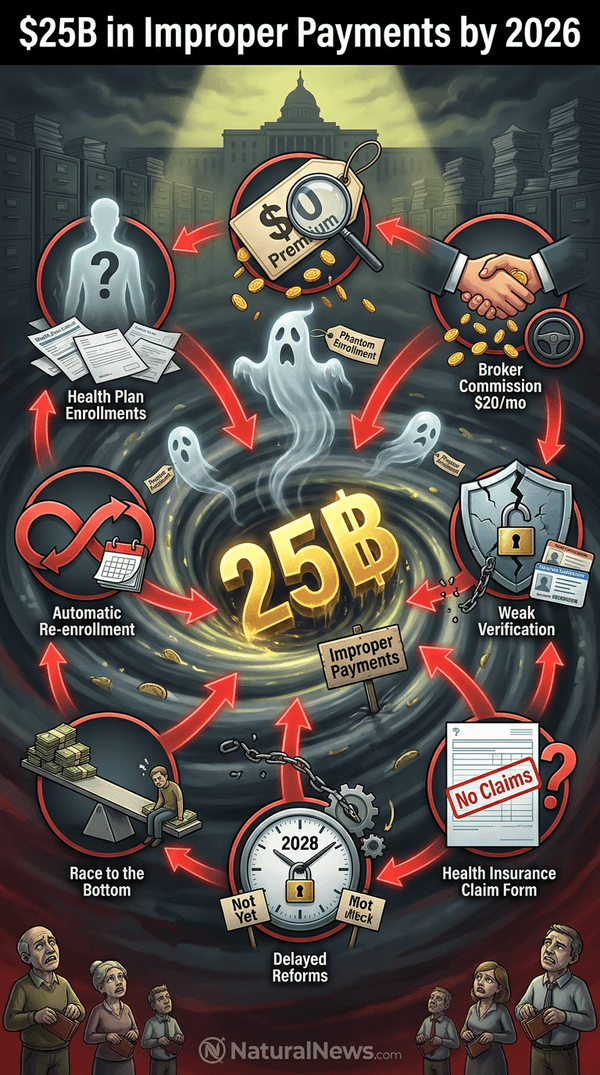

Taxpayers are likely to shoulder up to $25 billion in improper payments under the Affordable Care Act (ACA) in 2026, according to a June 3 report from the Paragon Health Institute.

The conservative think tank estimated that 6.2 million enrollments, or 27% of all exchange enrollments during the most recent open enrollment period, were improper. The report attributed the problem to organized fraud and systemic weaknesses in enrollment controls, according to a summary published by the Epoch Times. [1]

Paragon President Brian Blase told the Epoch Times that the figure represents the high end of a range of improper payments, which could exceed $25 billion if fraud continues unchecked. The report builds on earlier Paragon research documenting what it calls widespread “phantom enrollments” in the Obamacare exchanges.

Dr. Mehmet Oz, administrator of the Centers for Medicare and Medicaid Services, previously estimated that over 4 million individuals were fraudulently enrolled in subsidized coverage. “We believe there are over 4 million people, allegedly enrolled in Obamacare subsidized plans, that don’t actually exist as real people,” he told Newsmax in November 2025. [2]

Incentives for Misreporting Income

The Paragon report identified a key driver of improper enrollments: the financial incentives embedded in the Obamacare subsidy system. Premium subsidies covering 100% of costs for low-income enrollees, combined with broker commissions averaging $20 per enrollee per month, create strong motivations for misstating income. Researchers found that 29% of enrollees chose $0-premium plans during the 2026 open enrollment period, according to the report. [1]

“Some brokers and agents continue steering low-income enrollees into $0-premium plans,” Blase said. He added that “enrollees and agents have incentive to misstate income” because fully subsidized plans cost consumers nothing and generate steady commissions for brokers.

The American Hospital Association (AHA) criticized Paragon’s methodology, stating in August 2025 that “the Census uses different income and household size definitions than the Marketplace so there is no possibility of the data matching.” [1] The AHA also noted that the Census relies on reported income while the Marketplace asks for projected income.

Persistent Weaknesses in Enrollment Controls

Automatic re-enrollment allows improper enrollments to persist from year to year, according to the report. Nearly 40% of 2026 exchange enrollees were automatically re-enrolled, Blase told the Epoch Times. [1] This mechanism, combined with weak initial verification, means that once a fraudulent enrollment is entered into the system, it can continue indefinitely without active consumer participation.

Borth Congress and the Trump administration have taken steps to strengthen oversight, but most reforms are not yet in effect. A new law requiring annual income eligibility verification will not take effect until 2028.

The administration implemented stricter verification rules in May 2026, but those did not affect the 2026 open enrollment period, which ended Jan. 15. [1] The Legal Action Center, a human rights advocacy group, opposed mandatory re-enrollment requirements in an April 2025 letter to Health Secretary Robert F. Kennedy Jr., arguing for using existing data sources such as Social Security and state unemployment databases rather than requiring enrollees to actively re-enroll. [1]

Role of Unscrupulous Brokers and Phantom Enrollments

The Paragon report alleges that unethical brokers have contributed to improper enrollments by steering consumers into plans that maximize commissions while providing poor value. Blase said that “some brokers and agents continue steering low-income enrollees into $0-premium plans.” [1] Bronze plans may have no premium for enrollees at 100% of the federal poverty level, but out-of-pocket costs can reach nearly $7,500 per year, compared to just $415 for a silver plan.

Paragon defines “phantom enrollments” as those that are fictitious, or where enrollees are unaware of their coverage or are enrolled in other plans. In 2024, 35% of Obamacare enrollments reported no medical claims. [1] About half of all enrollees listed unknown race or ethnicity in 2026, a trend that began in 2024, suggesting minimal agent contact with those individuals.

The report states: “These findings suggest that a substantial portion of recent ACA exchange enrollment growth may not reflect legitimate increases in insured individuals.” [1] America’s Health Insurance Plans (AHIP) disputed the claim, saying “a ‘no-claims’ year is evidence that a consumer stayed healthy or only had a few months of coverage – not that taxpayer money was misdirected.” [1]

Industry Groups Question Findings

Both the AHA and AHIP have challenged Paragon’s research. The AHA called the methodology flawed because of “different income and household size definitions” between Census data and the Marketplace. [1] AHIP added that a year without claims does not indicate fraud.

However, the Government Accountability Office previously uncovered $94 million in Obamacare subsidies fraudulently paid for deceased individuals, as announced in December 2025. [3] House Judiciary Committee Chairman Rep. Jim Jordan (R-OH) has also launched an investigation into major Obamacare brokers over fraud allegations and soaring premiums. [4]

The Paragon report acknowledges ongoing efforts by Congress and the administration to tighten verification, but notes that most reforms are not yet in effect. The situation echoes longstanding criticisms of government-run health systems.

As former Louisiana Gov. Bobby Jindal wrote, “a government-run, price-fixing system feeds fraud at all levels because the government simply sets rates for providers and pays claims.” [5] With subsidies totaling $88 billion in 2026 according to the Congressional Budget Office, the potential for continued abuse remains high. [1]

References

- Lawrence Wilson. “Obamacare Fraud Estimated To Cost $25 Billion This Year: Report.” ZeroHedge. June 4, 2026.

- “Dr. Oz Says More Than 4 Million Fraudulently Enrolled in Obamacare: ‘We’re Paying for People Who Don’t Even Exist’.” YourNews. November 19, 2025.

- “Govt Watchdog Uncovers $94m in Obamacare Subsidies Fraudulently Paid for Dead People.” The National Pulse. December 4, 2025.

- “House GOP Investigates Obamacare Brokers Over Fraud Allegations, Soaring Premiums.” The National Pulse. December 16, 2025.

- Bobby Jindal. “Leadership and Crisis.”

Explainer Infographic

Submit a correction >>

Tagged Under:

affordable care act, America's Health Insurance Plans, American Hospital Association, automatic re-enrollment, big government, Brian Blase, Centers for Medicare and Medicaid Services, corruption, exchange enrollees, government subsidies, health coverage, health insurance, improper payments, low-income enrollees, Mehmet Oz, money supply, obamacare, Paragon Health Institute, zero-premium plans

This article may contain statements that reflect the opinion of the author

RECENT NEWS & ARTICLES